Money Printer goes 340Brrr

The ribbon cutting for a new pharmacy in Indianapolis embodies three underappreciated 340B dynamics

This May, a press release “celebrated the ribbon cutting of the newly opened HealthNet Pharmacy this week, marking a major investment in affordable pharmacy access, integrated specialty care, and medication support services for patients across Central Indiana.”

While likely not detected as a significant event to the casual reader, the opening of this specific pharmacy sits at the nexus of three underappreciated dynamics of the 340B Drug Pricing Program that are shaping the market for pharmacies and patients nation-wide.

“In-house” pharmacies owned by 340B Covered Entities (CE), not subject to Contract Pharmacy (CP) restrictions are, on net, quietly replacing other chain and independent pharmacies, and 340B is frequently touted as a “solution” to address the growing problem of “pharmacy deserts”.

340B CEs and State Medicaid budgets are in a zero-sum battle over the same dollars, which are called “340B Savings” by CEs and called “Forgone Rebates” by Medicaid.

For-profit corporations (other than CPs), often with financial backing from private equity or venture capital firms, are exploiting financial opportunities created by the spread between 340B acquisition costs and the regular prices of expensive branded prescription medications.

Let me explain.

340B CE-owned “in-house” pharmacies flourish as other pharmacies are rapidly going out of business

Starting in 2020, pharmaceutical manufacturers began placing restrictions on 340B CEs’ use of CPs. While CEs have since filed an ocean of litigation and passed laws in many States to fight against these manufacturer restrictions, the overall constriction on 340B drug purchase volume created two immediate outcomes.

First, pharmacies serving as CPs lost a significant source of profitability, as they were no longer able to acquire normally expensive branded prescription medications at the far-below-market-value 340B “Ceiling Price”, and thus could not earn the large margins associated with dispensing a 340B prescription.

Second, the manufacturer restrictions on shipping 340B products generally did not extend to in-house pharmacies which are directly owned by a CE. Thus, CEs looking to preserve or expand their significant 340B revenue streams, suddenly had a large financial incentive to open new in-house pharmacies.

Unfortunately, due to the suspicious data omission of the 340B OPAIS database not listing pharmacy National Provider Identifiers (NPI) under the ownership of each CE, it is very challenging to comprehensively track the growth of 340B CE in-house pharmacies.

However anecdotal evidence abounds of a trend of new pharmacies opening under the ownership of 340B CEs; sometimes the CE purchases a previously independent pharmacy and assimilates it (including aggressive sell-out-or-be-pushed-out tactics in some cases), sometimes the CE opens a new pharmacy in a neighborhood where previous independent or chains pharmacies closed, in some cases re-opening a pharmacy in the exact site of a previous closure.

Indeed, in Indianapolis the press release notes “the ribbon cutting comes as Indiana and communities nationwide continue to experience pharmacy closures and widening healthcare access gaps”.

As crushingly low reimbursement from the “Big 3” Pharmacy Benefit Manager (PBM) oligopsony continues to close pharmacies nationwide overall, the loss of 340B CP profitability may have tipped even more chain and independent pharmacies out of business. But those prescriptions still need to be dispensed somewhere.

340B CE-owned pharmacies have been happy to step in and take over the dispensing of those same prescriptions, which were unprofitable or even money-losing for most regular pharmacies, but are still highly profitable via the in-house pharmacies’ government-granted lower acquisition costs.

While it is highly unlikely the “intent” of the 340B program ever involved creating a structural survivability advantage for pharmacies owned by non-profits that qualify for 340B, over their competitor pharmacies that are simple businesses, in 2026, that is the outcome regardless.

In State Capitols, 340B CEs wage lobbying wars to protect “340B Savings” that are earned at the direct expense of State Medicaid budgets.

Further down in the press release, it notes: “Indiana’s recent decision to exempt Federally Qualified Health Centers (FQHCs) from proposed Medicaid-related 340B drug pricing restrictions.”

This references a dynamic created by the Duplicate Discount Prohibition in 340B, where “manufacturers are not required to provide a discounted 340B price and a Medicaid drug rebate for the same drug.”

In States that administer Medicaid benefits via Managed Care, this has resulted in 340B CEs gaining the ability to “front-run” Medicaid budgets, by claiming the 340B discount immediately at the point-of-sale, and forcing the Medicaid program to forgo the usual rebate, resulting in a complicated and opaque net transfer of dollars from the State Medicaid budgets to CEs. This dynamic has now been well described in academic research, industry funded general research, and think tank articles.

Earlier in 2026, Indiana’s Medicaid program proposed ending this front-running; however, after intense lobbying from in-state CEs, the proposal was adjusted to end the front-running by hospitals (which represent the large majority of dollars involved) while allowing FQHCs (including Healthnet) to continue earning the “340B Savings” at the expense of the Indiana Medicaid budget.

Had the initial policy proposal not been amended, the new pharmacy may have never opened; as much of their patient base is likely covered by Medicaid and if the pharmacy had been unable to earn “340B Savings” on those patients’ prescriptions, the operations of the pharmacy may likely have shifted from black to red.

This zero-sum game over the same dollars between CEs and State Medicaid budgets will be something to watch in dozens of State Capitols in the near future; as State Medicaid budgets will be strained under the ramifications of H.R.1, legislatures and Medicaid programs may likely decide they need to reclaim these dollars that have benefited CEs up to this point.

This is not an insignificant amount of money, the Indiana proposal noted $60 million per year, and a recent report from Minnesota showed the CEs in that State earned $261 million in 2024 at the direct expense of the Medicaid budget. One State legislator referred to these funds as a “hidden subsidy”, and going forward it is possible in many states the funds will no longer be hidden nor a subsidy.

For-profit corporations continue in numerous creative ways to exploit a government program intended to assist non-profit safety net health care providers.

Lastly, the press release references: “AndHealth helps Community Health Centers (CHCs) radically improve access and outcomes in specialty care for patients, providing everything CHCs need to deliver in-house specialty care and specialty and retail pharmacy, built for the unique needs of our medically underserved populations.”

As well as: “AndHealth is supported by key investors including the American Medical Association’s innovation subsidiary, Francisco Partners, and the state of Ohio’s economic development organization.”

So, who is AndHealth and how do they fit into this story?

AndHealth is a for-profit firm founded in 2022 by “former CoverMyMeds co-founder and CEO Matt Scantland and the team that helped grow healthcare technology company CoverMyMeds from inception to its $1.4 billion acquisition by McKesson in 2017.”

The new firm was founded with funding from Francisco Partners (a private equity firm) and Health2047 Capital Partners (the American Medical Association’s venture capital arm) and, given the timing following the 2020 manufacturer restrictions on 340B CPs, it’s possible the entire point of AndHealth was to capitalize on the favorable financial dynamics associated with CE in-house pharmacies.

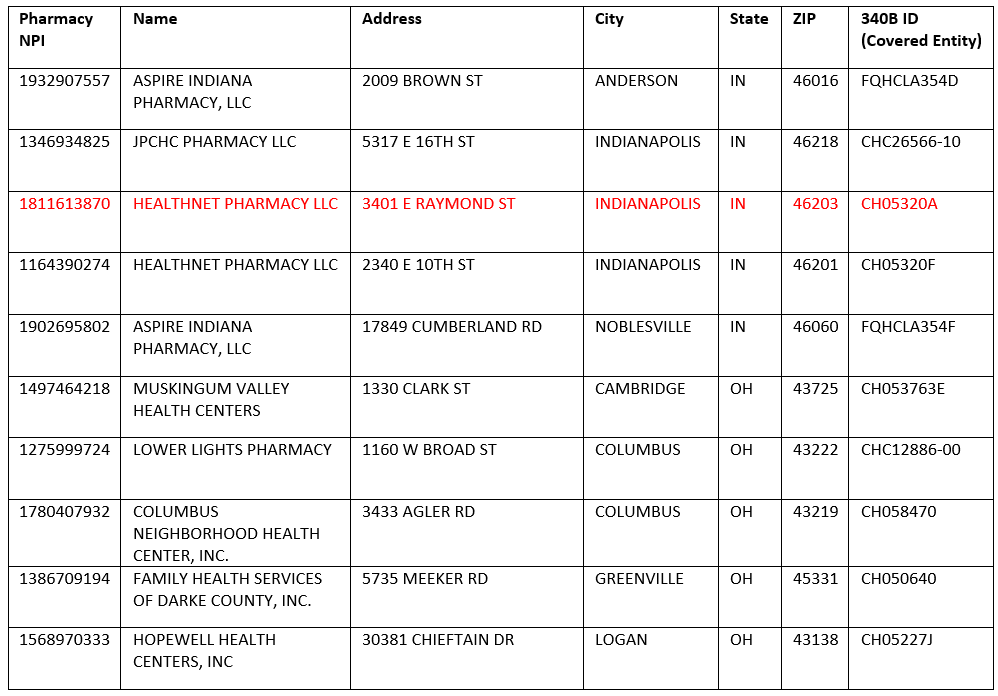

Interestingly, if you navigate the “Specialty Pharmacy” page at the AndHealth website, it identifies 10 pharmacies as “AndHealth specialty pharmacies”:

However, upon further investigation of the pharmacies (Pharmacy NPI and 340B Covered Entity IDs are public information, searchable at public websites), all these pharmacies are not owned by for-profit AndHealth but instead are owned by separate individual HRSA-funded health centers, each participating in 340B.

The newly opened pharmacy from the press release is highlighted in red.

As such, unknown portions of 340B revenues earned from this newly opened non-profit pharmacy, along with the other nine pharmacies, will flow (at a minimum) to a multimillionaire founder, a venture capital firm, and a private equity firm.

Conclusion:

The perverse incentives embedded in the structure of the 340B Drug Pricing program and its stratospheric growth over recent years have thrust the previously obscure government program into the public eye. While much attention has been given to the effects of 340B on hospitals, pharmaceutical manufacturers, and health plan sponsors, less attention has focused on the warping effect that 340B has had on the pharmacy market and patient geographic access to medication, State Medicaid policy decisions, and the multiplicity of ways that creative for-profit firms have found to financially exploit the program.

When Congress eventually reaches the critical juncture for 340B reform, or ending the program entirely and replacing it with targeted direct appropriations to safety net providers, it should consider these underappreciated 340B dynamics, perfectly embodied by a single new pharmacy on the east side of Indianapolis.

Another sharp one, Ben. I'll own it: I run field ops for a health system specialty pharmacy, so I'm part of the in-house dynamic you're describing here. You're still right. The one thing I'd add from the inside is that in specialty the volume we capture tends to come off PBM-owned pharmacies more than independents, but that doesn't undo the structural problem you've laid out so well. Appreciate the work as always.

Well written Ben ! Nice job.